Spotify ("The Swedish Netflix") reports, essentially while we are sleeping tonight. The Podcast King is expected to to report revenue growth of about 20% at $4.6b and earnings of $2.52-ish or more, which is a growth rate too large to really delve into here. Not because it isn't impressive but because I don't think it matters all that much what Spotify reports as much as how they guide.

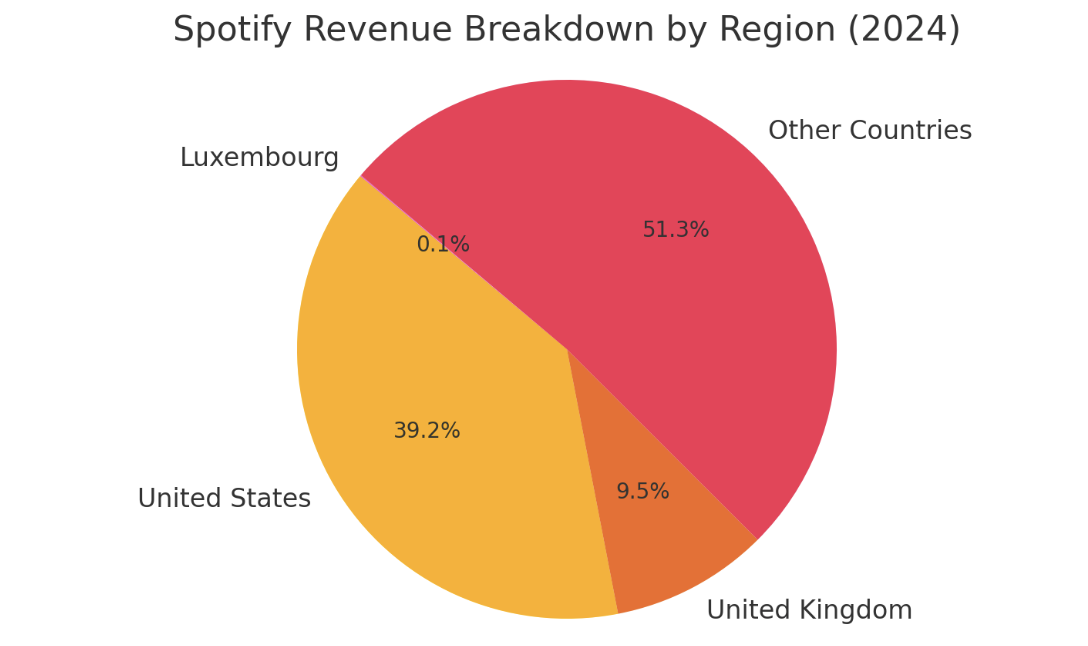

Spotify isn't cheap for the best reasons. 1. The company is now printing money and utterly indispensable to ~265 million people worldwide. 2. There isn't (yet) a tariff on steaming stuff 3. Spotify is a global brand, generating more than half its revenues from "other countries" (there are apparently consumers in non-America, I'm having a team look into it).

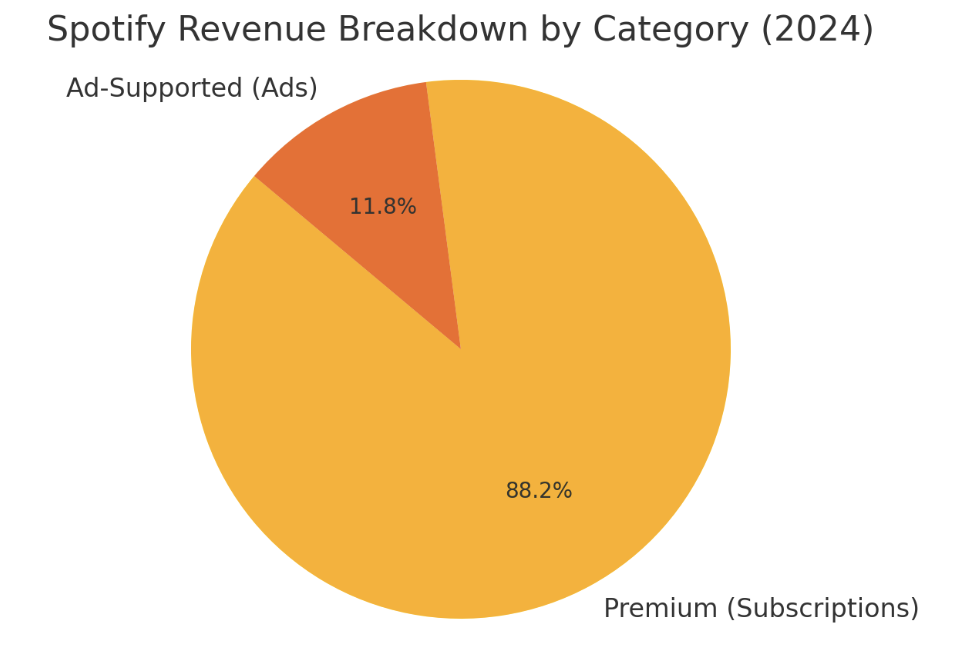

While we're pie-charting let's add this:

That's Spotify's revenue breakdown on advertisements vs subscribers. Combine those two ChatGPT-generated charts and my hand-written efforts and you know why Wall Street was comfortable bidding SPOT up 33% YTD while the rest of the world burns:

Ads are flaky but Subs stick around. This is a big part of a lot of my investment thesis this year. I think the supply chain, small retailers and the incremental employer are sort of screwed in a large but unknowable way. But I also think the center holds. I don't believe we will be plunged into a Global Depression by trade. Advertisers can leave and Spotify will make up the difference by creating podcasts about how Liberation Day stacks up on the list of Greatest Unforced Errors in Political History (Answer: somewhere behind invading Iraq and Teddy Roosevelt promising not to run for a second term).

Consumers under pressure will stop spending out of the house but they will hold on to their comfort home-front goods.

Unless Luxembourg goes to hell Spotify should be fine, barring a 1930s-type of outcome. Subscribers will dump Hulu, Disney+, Amazon Music and about a million other things before you pry Netflix and Spotify from their under-funded fingers.

I'm grading Spotify on three metrics, the first of which is the most important:

Global Premium Subscribers. The trailing number should beat, guidance will be uncertain but only out of prudence as opposed to concern.

Messaging. SPOT isn't immune to the vicissitudes of fate and Presidential whims but it's got a hell of a business model. I spent 4 years on TV and another 3 doing online stuff. You know what gets clicks? Human misery. Spot sells comfort music and podcasts. "We win no matter how much people suffer" should be the underlying message from Spot.

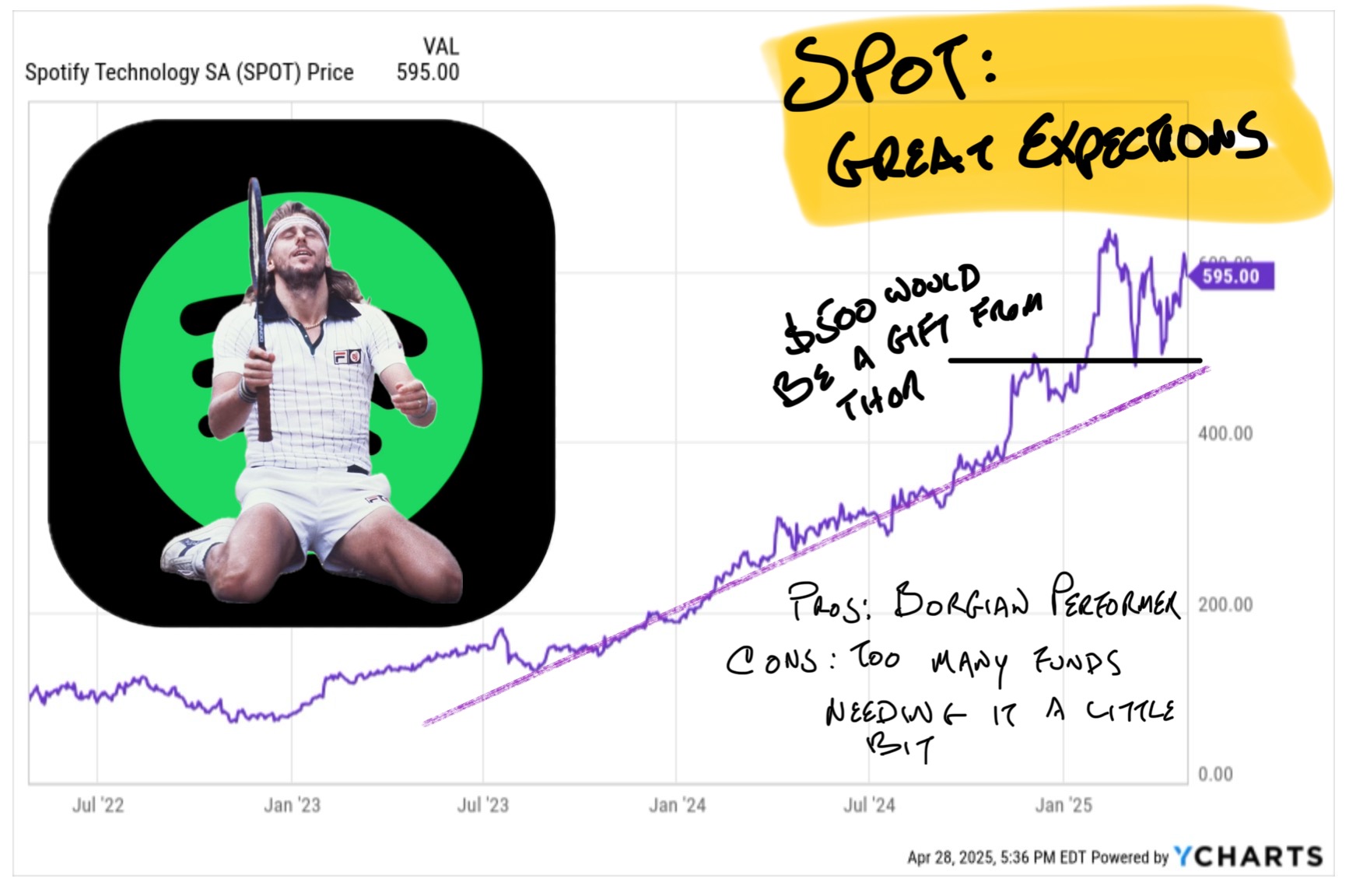

Bonus for actually having the Lutefisk to raise the subscriber outlook for this year. I'm looking for Spot to be a corporate Bjorn Borg. Soft-spoken but confident. Looking good in a time of global chaos and working like a psychopath behind the scenes.

Strategy

SPOT is a suddenly super crowded long, especially since Netflix reported. I'm apparently not the only one who noticed the similar nature of the businesses. If the company somehow screws it up tomorrow I'm a buyer. $550 is great. $500 is amazing. Honestly, without an accounting scandal or the revelation that 75% of Spotify's profits are somehow being created in a Chinese sweat shop this is a stock I want to own.

There are a lot of fund types who borderline "need" SPOT to crush. That's a dangerous mix. It also tends to dampen the volatility for complicated math reasons that boil down, in human terms to "Wall Street will find the most desperate holder and smash him to death then find the next most desperate holder..." and so on until everyone breaks even.

Beat, guide higher, stock down: Buyer

Beat, guide higher, stock flat: Slow Buyer

Beat, guide lower, stock flat: Buyer

Miss, guide lower, stock down: Buyer

Dream/ nightmare scenario: Add half a lot at $550. The rest at $500 then work Rosary beads. No need to chase in this tape.

Report card for SPOT tomorrow. So far Hasbro and Mr. Monopoly are the top students in my Consumer Universe with the A- posted last week.