Home Depot is getting the headlines but there are better trades below the surface

Home Depot is who I wrote about them being last night; a great American company more or less chained at the neck to the US housing market. This morning HD shares are higher by a couple percent after the company reported positive comps for the first time in 2 years and slightly better than expected guidance.

Listening to the call as I type. The company is taking share, where possible and continues to invest in the business. HD can make you money if you get long during periods of housing recovery but, well, we're not there yet.

Senior Exec VP Ann-Marie Campbell and CEO Ted Decker on the HD Analyst call just now:

"We continue to see softer engagement in larger discretionary projects"

"The higher interest rate environment continues to pressure larger remodeling projects"

"Our customer is very healthy... as they stay in their houses longer they will take on larger remodeling projects as opposed to moving [but not yet]"

So, HD is a blue chip in decent long term shape but isn't really going to do much better than flattish comps until the environment improves.

HD is a decent proxy for housing and a very specific segment of the consumer. That's not nothing but not enough that I'm going to spend a ton of time on it here. Someday maybe we'll talk about the super interesting story of HD. But not this day.

Callaway TopGolf: Is it time to a shot at this iconic dumpster fire?

Conservative investors can probably do fine getting long Home Depot here. Which is fine. But a good portfolio of stocks (as opposed to more passive ETFs which most people should own) has a mix of Blue Chips and broken down, shambling messes that have been given up for dead by the rational investing world.

There are few things less rational than golf. Golf courses are ecological disaster, an elitist moral quagmire at every level and barely even exercise if you don't carry your own clubs. Golf was invented ~600 years ago by a bunch of Scottish sheep herders and equipment hasn't been a growth business since a surly prodigy named Elderick Woods won 4 Majors in a row 25 years ago (which is also when TV ratings peaked).

But here's the thing: golf isn't dying. It's actually growing. Not as a sport people watch on TV or talk about in mixed company but as a hobby Americans take part in. In 2020 the pandemic pushed rounds of golf played in the US over 500 million for the first time since Tiger Mania's 2002 peak.

There are fewer on-course golfers now (~30 million in 2002 vs 28.3 today) but off-course golf has exploded into existence through simulators and the fading TopGolf fad the number of people who golf exclusively at driving ranges and simulators hit 10 million last year, a 10 fold increase over 20 years.

In light of all that you'd think a company selling the most popular gear in golf AND leading off-course industry by far would have made a tremendous investment.

As it turns out, nope:

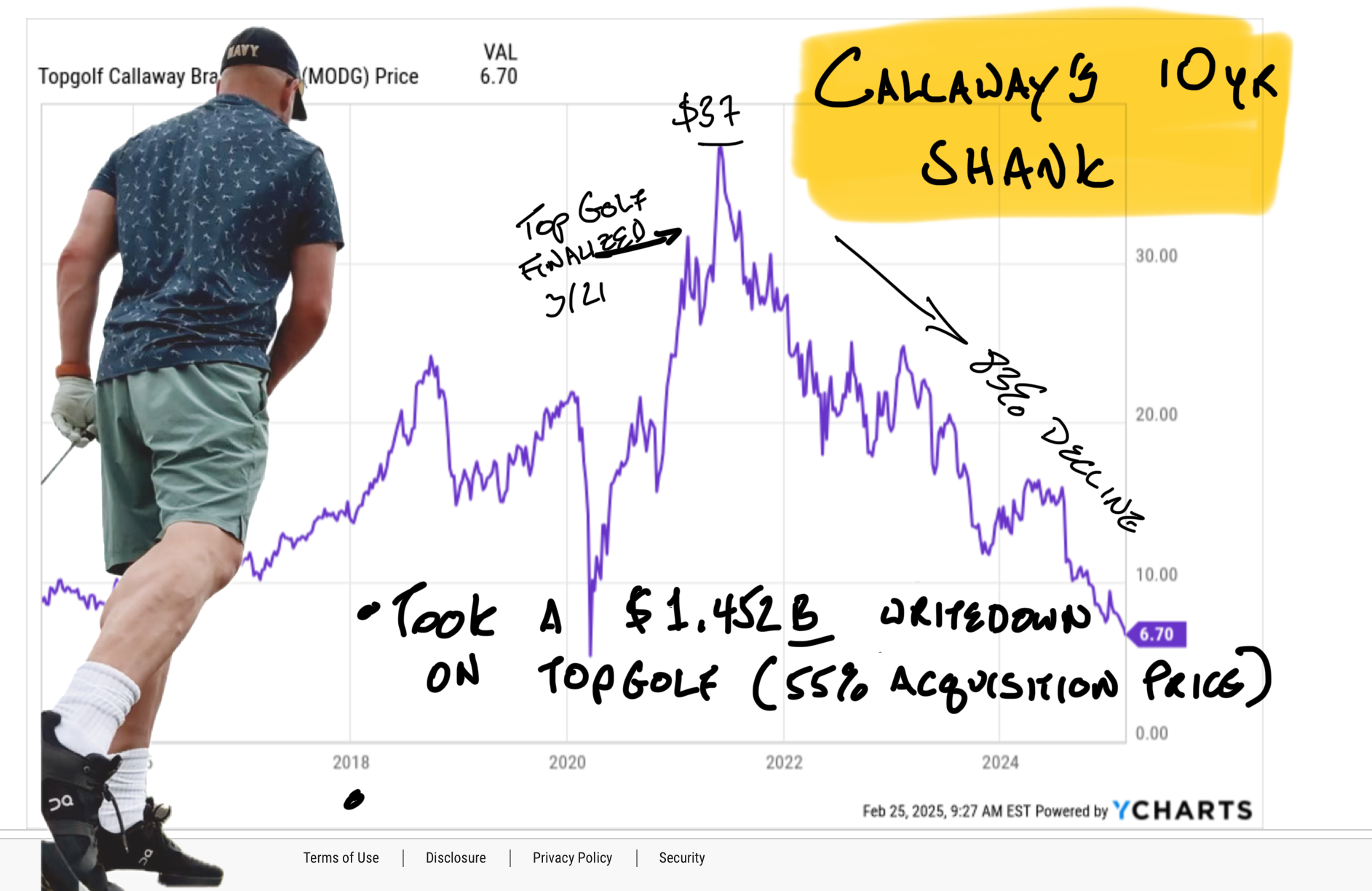

Topgolf Callaway Brands Corp ($MODG) has the best selling clubs in golf, the second best selling golf balls and a moderately profitable (though poorly run) apparel business. Yet the investment has been a disaster by almost any measure. $10k invested when the company went public in 1992 would be worth $16k today (vs ~$270k if you'd invested in the S&P500 at the same time).

What happened? A little hubris, a spot of bad timing and the kind of half-ass investment decisions often seen at these smaller cap companies run by not-particularly-motivated folks.

It shouldn't have gone this way for Callaway. Not only did the company re-invent driver technology (a process which has gone comically far) Callaway management had the foresight to be one of the first outside investors in the Topgolf, the chain of driving range/ entertainment centers driving the adoption of of-course golf. In 2006 Callaway bought 20% of Topgolf for about $25 million. In 2017 Callaway wrote up that investment to ~$290 million, implying about a $2.1 billion value for Topgolf.

Callaway was doing about a billion in revenue in 2017. Turning a $25 million Topgolf investment into stake worth $290 million was a great score for Callaway. Remember, this is a company making golf clubs. They have a legendary facility in Carlsbad where pros will hang out and tweak clubs and generally golf-nerd out with the best possible toys. Profits were fine. Tiger Mania was over but clubs were a great core business. Pretty much any guy going from middle to upper-middle class was like 95% to buy clubs at some point in his life, most of them from Callaway.

Callaway wasn't a great public company but hanging out in Carlsbad, making clubs and sticking to what they knew had been working just fine. Callaway's stake in Topgolf was the equivalent of of ~3yrs of cashflow, all from a $25m investment. Let it ride, cash out and buyback stock, make clubs mind-bendingly long drivers and party like golf junkies in Carlsbad. It sounded sweet then and still does now.

Callaway went a different direction. In 2020 Callaway bought out Topgolf in a deal valued at a little over $2 billion and assumed another $555 million in debt. CEO Chip Brewer declared Topgolf "the best thing for the sport since Tiger Woods" and decided a background in selling stuff out of golf proshops (by now Callaway was making balls, shirts and clubs) pretty much made running expensive driving range/ bars in converted parking lots a lay-up.

It went great at first. Then not-great.

The Here and Now

Last night Callaway reported great results in golf equipment (up 12%!) and wrote down the value of Topgolf by $1.45 billion, which is more than half what Callaway paid for Topgolf 5 years ago. So that's bad. It's also awkward because late last year Callaway announced it was going to unwind the merger and spin off Topgolf in a manner to be determined.

What last night's announcement makes clear is Callaway won't be selling Topgolf for $2.6 billion. But rational people already knew that. Callaway shares opened weak but are currently flat, a couple hours into the day. I think they might go positive.

Callaway's impairment charge doesn't hit cash or cashflow. Topgolf's comps are garbage (-9%) and likely to stay that way longer than the company thinks. It's not clear why Callaway is even in the apparel business when the margins are mid-single digits. The company just got done digesting a sales disaster at a UK outerwear company. WTF does Callaway have a British outerwear company? Maybe selling chicken wings, $15 drinks and time in the driving range was too easy. Who knows?

There's a reason MODG trades at an EV to book of 5x. Callaway is still good at golf clubs. Everything they do that gets them away from anything that isn't golf clubs is good. They aren't running out of cash.

There's money to be made today. It's not in trading Home Depot up 2%. It was in getting long the poorly run golf company down 8%.