It's Game Time. By Tuesday morning's opening bell earnings from Target, Best Buy and ON will have set the stage for the coming flood of retail earnings... if you know what to look for. How to get ahead of the wave.

It's time to get serious about retail earnings. Walmart has doubled the performance of the Magnificent 7 over the last 12 months. Right here in this very space I suggested buying the dip when the stock sold-off on weak guidance. And Investors who did chalked up gains of about 3%.

I love the consumer, Walmart the stock and making money but not even I can get super fired up over grinding out 3% trades on the largest employer on earth that isn't the Chinese Army. The entire planet follows Walmart and Amazon. If you don't own the stocks you should. And, once you buy it's best to forget about them entirely.

If you want to make money trading consumer stocks you need to get into the grit and draw conclusions where the rest of the world doesn't. It requires knowing not just the financials but the stories behind some of the three-legged dogs, fallen angels and more obscure companies just popping up on Wall Street radars.

We hear from three companies punching well above their weight in terms of information value before the bell on Tuesday. Let's take them in the order they report and tell you why they matter.

$ONON: 5am

Leading off from company HQ in Switzerland is the awkwardly-named clothing up and comer ON (popularly referred to as "On Cloud" because of it's most popular shoe, "ONON" because of the ticker and "Cougar Shoes" because ON had about 75% of the hot mom market before your dads and teens even heard of the brand).

Foreign domiciled athletic fashion brands trading at 50x earnings might not be your bag. And fair enough but if you've missed the "Short Nike, long Anyone Else" has been absolute cash-money for the last 3 years:

Nike is a $55b company with eroding top and bottom lines for almost half a decade. ON and Deck's Hoka brand have been the highest margin beneficiaries of the trend, selling top-price shoes and very seldom offering discounts. ONON shares aren't pricey because investors are insane (necessarily). It's expensive because ON is growing revenues at >30%, is still not even doing $2 billion, just posted 75% growth in Asia and has enormous runway over the long term.

But... and it's a big but, the "Long Everyone But Nike" trade broke pretty sharply over the last month when a so-so forecast from Deckers tanked the space. In the meantime Nike shares are taking on a bit of a Starbucks vibe ("new CEO, no expectations, doesn't have to be 'great' just better than terrible"). In a risk-off market you'll make more money being long Nike than you will a basket of growth shoe cos.

Position: Long and nervous about ON.

Names to watch and trade off ON's results: $SKX, $DECK, Adidas.

Wildcard: Foot Locker, which reports on Wednesday. About half of FootLocker's business is still Nike-related shoes and apparel. FootLocker has been an unadulterated disaster for almost a decade, both because it's not a good company and also because it depends so much on Nike.

If ON misses watch for a dip in FL. Such a dip might be a good long spec.

Target: 6:30 AM

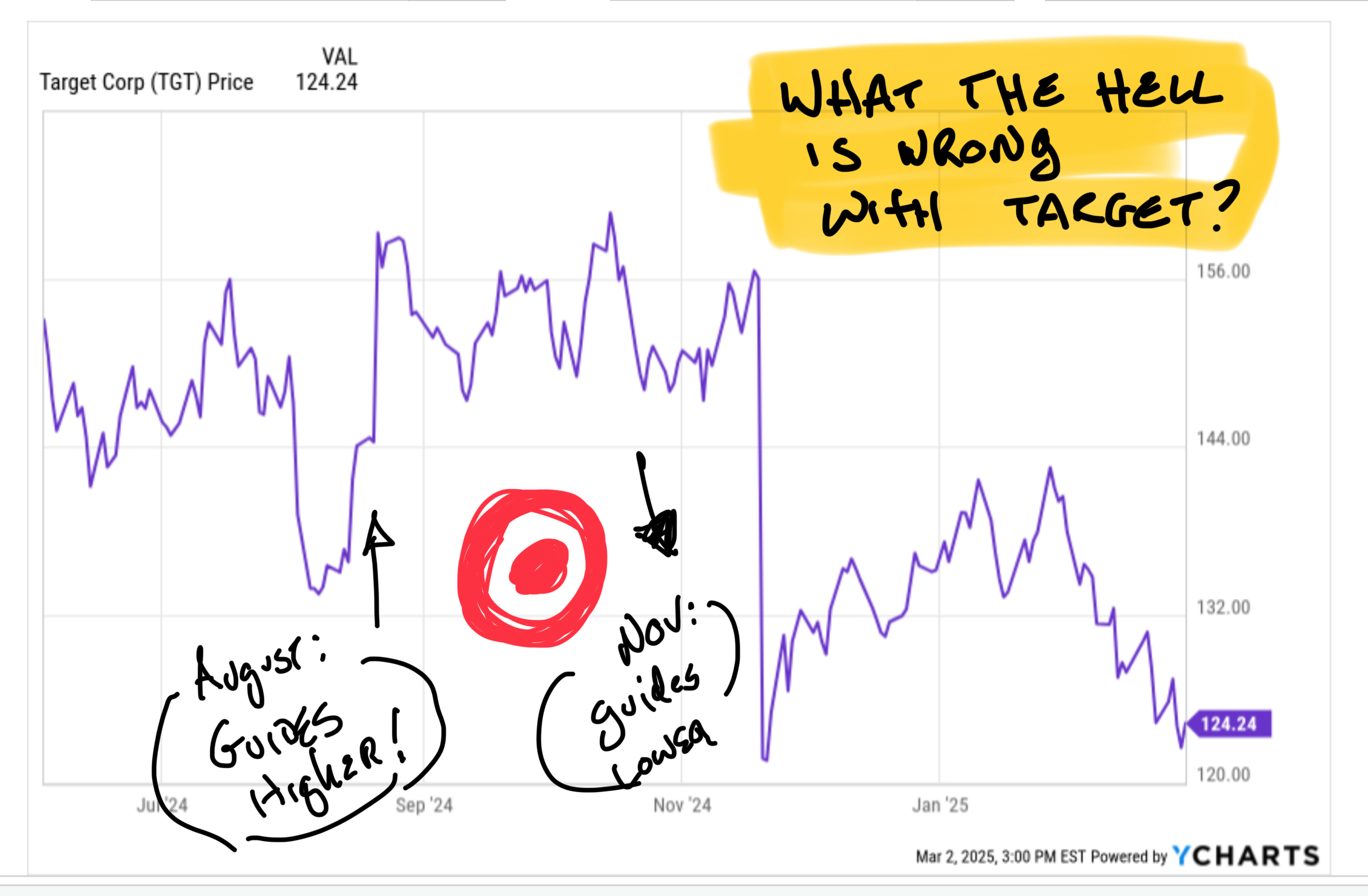

I think and talk about Target more than the company has frankly deserved over the last few years. Expectations for Q4 and frankly the foreseeable future aren't great. This was shocking 3 years ago when Target, then trading at $260, took guidance lower for Christmas 2021.

Now the stock is near 52-week lows at about $120. Last quarter Target guided lower 3 months after guiding higher. Honestly, taking down numbers three months after you raise is such a screw up there's not even a term for it. If a major company in reasonably predictable business is ever lost enough to raise guidance in August then reverse the outlook to below where it started in the first place again it will be called "Pulling a Target".

But Target still matters. Mostly because Target has its fingers in all sorts of different consumer pies. Target will do at least $100 billion in revenues in 5 different categories, each of which has its own trades.

Target does about $17 billion in apparel sales. We hear from Victoria's Secret (which has been on a heater) and Gap (which I own) later this week. If Target was just a specialty clothing retailer it would be among the biggest on earth. Lost or not, what Target says about discretionary spending should color your thinking about VSCO and GAP later this week.

Target also sells about $35 billion of "Beauty and Household Essentials", a decent chunk of which comes from a store-within-a-store ULTA partnership and fast-growing ELF. Elf is down 70% in less than a year after being more than a 10 bagger since the start of 2021. Make-up in general has taken an unreal beating from EL to ULTA. Elf loves to talk about the Target relationship but Target never mentions ELF. If you're hoping for a bottom in make-up generally or ELF in particular you better have Target data to back it up.

Target dabbles in a little of everything from clothes to TVs (though not very many of those these days). The company needs a new CEO, a bit of fashion luck and maybe another lockdown to be a compelling long but it's still required listening if you want to know what's up with US consumers.

Position: In Target? Noooooo... but gun-to-head "not bullish"

Names to trade off Target news: ELF ULTA GAP AEO VSCO PEP BBY COST

Wildcard: A new CEO (Brian Cornell is already assumed to be retiring at the end of this year, "sooner" would be welcome at this point). Bad news has been rewarded when expectations are low. And wow are expectations low here.

I personally would be the most bullish if Target stole the CEO from...

Best Buy: 7am

Best Buy sells televisions, computers, phones and other things that are easier than ever to buy online, you don't need to replace very often and you probably just upgraded a couple years ago.

Home Depot says they aren't seeing bigger ticket projects. Walmart says the consumer is still cautious. Best Buy themselves expects negative comps and yet another year of promotional pressure ahead.

Obviously you can trade almost anything electronic or even home related off Best Buy but I'm mostly including BBY here because I believe two things that I don't here elsewhere about BBY:

CEO Corie Barry is a stud. She's made Best Buy a much, much better company in her 6-odd years at the helm. She's going to get stolen by a bigger merchant if Best Buy isn't careful.

Best Buy is going to take enormous amounts of marketshare in almost everything they do when the housing market turns. Which isn't going to happen just yet but will in time. Discount stores aren't set up to sell TVs at anything other than rock-bottom prices in a post-COVID world. Best Buy has overcome shrink by driving almost half the business to online, changing the lay-out of stores and improving service.

Super smart. The stock will lead the comeback and a lot of people are short. Watch the reaction to what will probably be lousy news from Best Buy.

Huge week and more trades I can really cover here. Load up on coffee, get your sleep and sign up for this newsletter. It's going to be a crazy couple weeks.