Bottoming is best thought of as a process rather than a moment. The all look different but when you see a correction it usually hits these stages:

A negative catalyst appears, usually when stocks are expensive. Expensive stocks get sold. Investors "rotate" with growing speed.

The threat seems larger. Inevitable. The rush to the exit picks up pace in stocks. Everyone's running the same playbook and "sell" is the only defensible call as every group sells-off.

The tide turns, slowly then all-at-once. The risk becomes quantifiable. Bad news becomes more company specific. Selling slowly dries up as (dirty truth of investing here): The Optimists Always Win.

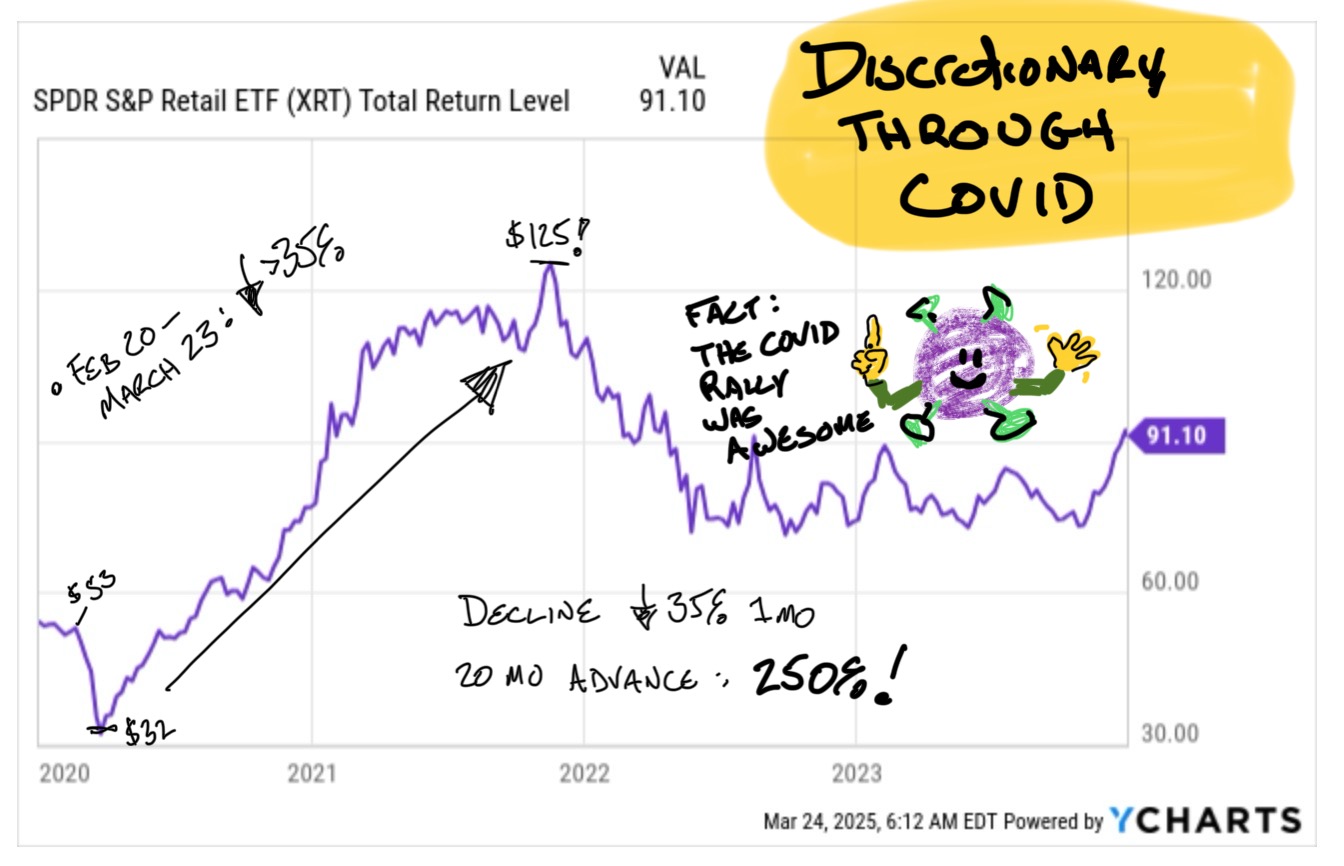

That was the case to a much greater degree the greatest bottom in the history of consumer discretionary stocks in March of 2020. The group was down 35% in just over a month. Stores were shutting down day after day, leading to pretty much the entire economy being shutdown for the foreseeable future.

It was a really hard time to start buying consumer discretionary stocks. Like a Trade War the idea of closing down the entire economy seemed like a serious headwind for mall stores selling ~20% of their stuff online, usually through insanely inefficient, margin killing systems.

This isn't COVID. But it's not totally different. Tariffs of Unknowable Size kick in next week. The impact is literally unquantifiable because there are no rules. At all. It might all be a head-fake. Or it could lead to a debilitating trade war.

Here's the thing. This is still America. This country has endured quite a bit and until recently stocks were at all time highs. Retailers that aren't dead yet have by definition gotten wildly better at sourcing and dealing with using multiple sources. AEO management rather famously bungled distribution during COVID (over buying shipping capacity at the top, intending to sell the extra space for even more money).

This time around the same management team responded to the trade threat with a shrug. "Where we supposed to be going?" the CEO asked. "We ship from China, India, Vietnam. Tell me where the cost will be lowest."

Which is what Unquantifiable Risk Means but also a pretty rational response by the company. Good enough to get me long, after the decline AEO has seen.

The Tariff deadlines are getting less scary but, either way, there will (possibly) be rules next week. The risk will be known. Consumer Discretionary as a group was down 20% in a couples months. The damage for cos seen as less resilient (more susceptible to a recession) was worse than that.

We've priced a whole bunch of misery into these stocks. We saw clear signs of that on Friday.

The Selling Drying Up:

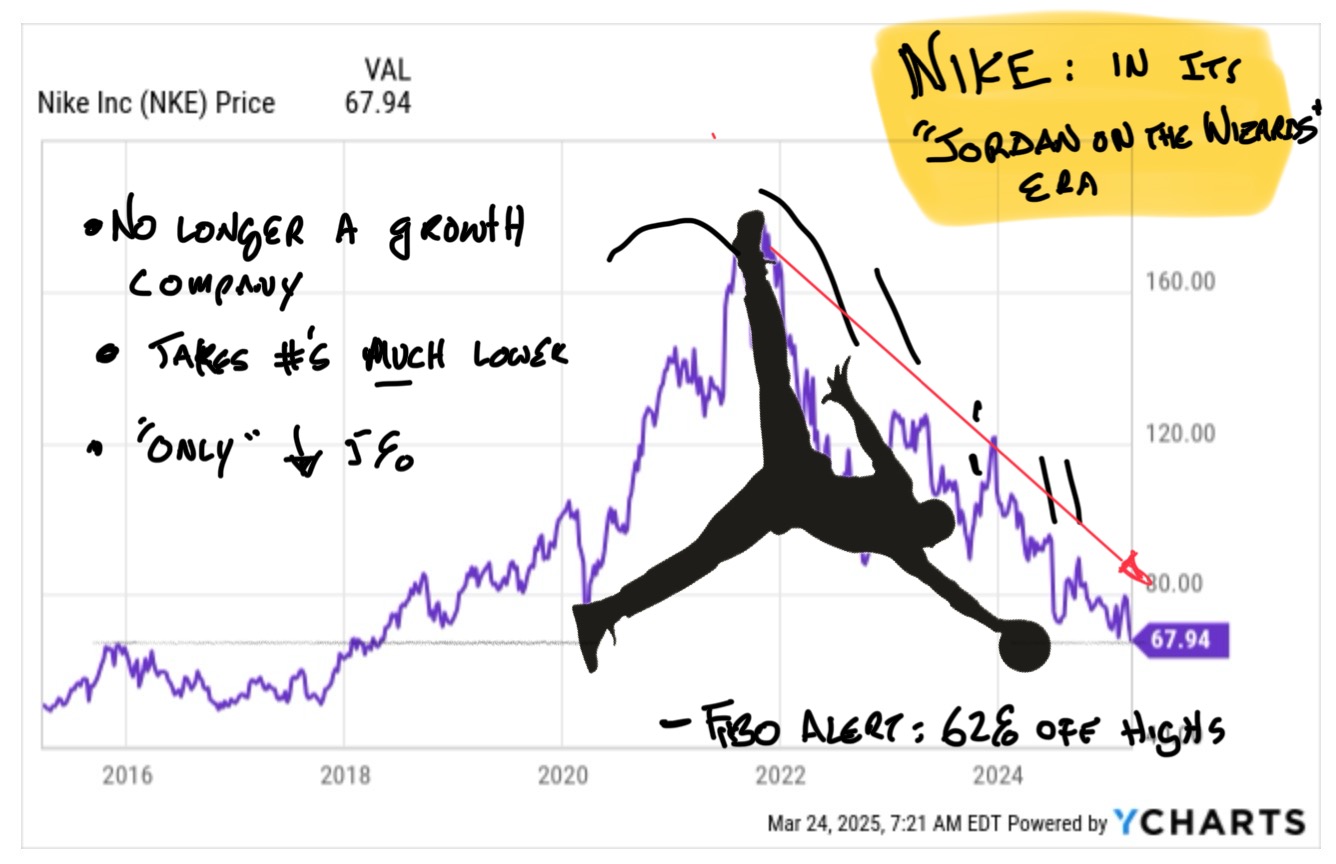

Last Thursday I created a basket of Indefensible Stocks. 10 stocks, 10% in each, names no one loves. Lamentably, the list included Nike which blew up and threatened to take the whole mall with it on Friday morning.

Nike really was terrible. After spending years pissing off retailers and withholding supply Nike is having a hard time getting the shelf space back. Oh yeah, the co is still creatively sort of... dead. They missed the athleisure era, which is almost unimaginable. Honestly, Lululemon wouldn't exist if Nike had been paying any attention at all.

Nike's report was bad enough to taint everyone, at least lately. And early in it looked like another bad day. Carnival Cruises reported a great quarter and openly laughed at the idea of a weak consumer (in the nicest way). "We're selling tickets at the highest prices ever and the list is the longest it's ever been, onboard spending is still great and we're not seeing cancellations". Shares fell 5% anyway and figured to keep going lower. Because "recession".

But Carnival shares rallied back to flat and it was a portent of a decent day in these names, even before yet another Tariff shift. By the end of the day, the Indefensible basket finished higher after opening down 3.4%.

Here's how my trade ideas from last week performed.

You need to have a subscription to access this content in full.